Debt-to-Income (DTI) ratio is a critical metric that lenders use to evaluate a borrower’s financial health when assessing loan applications. It measures the percentage of an individual’s monthly gross income that goes towards paying off their debt obligations. A high DTI ratio indicates that the borrower may be at risk of defaulting on their loans, while a low ratio signifies that the individual is in a strong financial position. Understanding your DTI ratio is essential when managing your finances, and it can help you make informed decisions when taking on new debt or managing existing debt. In this blog post, we will delve into what a DTI ratio is, how it is calculated, and why it is an essential factor for lenders and borrowers alike.

When you apply for a boat loan, your marine lender will review your financial history to determine whether you’re a good candidate for borrowing. They’ll look at your credit score, your payment history on other loans or credit cards, and your current level of debt compared to your income. A low DTI indicates that you have a manageable level of debt relative to your income. This is important because if your DTI is too high, lenders may be hesitant to approve your loan, as it suggests that you may struggle to keep up with payments. At Trident Funding, we can work with you to understand and improve your DTI so that you can increase your chances of getting approved for a boat loan.

Debt-to-Income Ratio for Boat Loans

What is DTI?

Why DTI Matters

What is a Good DTI?

What Should My DTI be for a Boat Loan?

Ways to Reduce DTI

What is DTI?

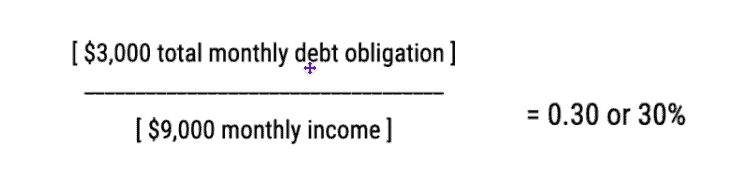

A debt-to-income ratio, or DTI, is used to compare your outstanding debt burden to your current income. To calculate this number, you’ll need to add up all of your monthly debt obligations, such as your total loan payments and the minimum due on your credit cards or other revolving lines of credit.

Then, you will divide that minimum monthly requirement by your monthly income. The resulting percentage is your DTI.

For example, let’s say that you have a net monthly income of $9,000 and you are required to pay $3,000 per month between your credit card, auto loan, and mortgage loan. In this case, you have a DTI of 30%.

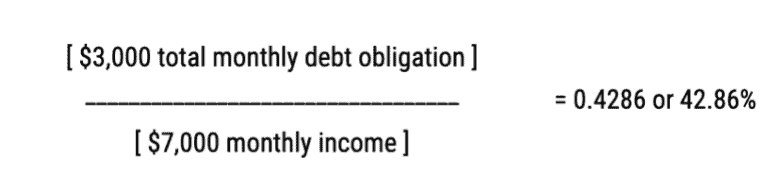

Now, let’s say your debt stayed the same but your monthly income was $7,000 instead. In this case, your DTI would rise to just under 43%.

The higher a DTI, the riskier a borrower may appear to a lender. That’s because they have less available income to handle unexpected expenses and situations, and run a greater risk of defaulting on the loan (failing to make payments on time or repaying the debt in full).

Why DTI Matters

The purpose of a lender is to finance purchases for qualified borrowers. Before lending them money, however, lenders must analyze a borrower’s financial health.

This means looking at overall risk factors and determining whether or not the borrower is likely to repay their debt as promised. In addition to income, credit score, and payment history, one important factor that lenders will consider during this process is a borrower’s DTI.

Though your debt-to-income ratio is just one possible factor, it’s an important one. That’s because it gives lenders a good idea of how much debt you owe relative to your unique income and budget.

It might not be such a big deal to have $6,000 in monthly debt obligations if a borrower brings home $50,000 per month. After all, that only accounts for 12% of their income. However, if a borrower is paying $6,000 toward their debt each month out of a $10,000 net income, they have a lot less discretionary income to work with (and a DTI of 60%!).

That difference is why DTI is so important to lenders. Simply looking at a potential borrower’s existing debt doesn’t offer the whole picture. It’s imperative to look at how much of the borrower’s monthly income is already spoken for, and what one can realistically afford to take on with a new boat loan.

What is a Good DTI?

Each lender sets its own requirements for things like credit scores, down payments, and DTI. A debt-to-income ratio that’s acceptable to one lender might be too high for another, especially if other borrower requirements are not met.

A “good” DTI also depends on the product you’re trying to get and whether your debt will be secured or unsecured. For example, a home mortgage lender may allow for a higher DTI than a personal loan lender, simply because the mortgage lender can hold the property as collateral and simply foreclose on a defaulted loan. With an unsecured debt — such as a student loan or personal loan — lenders may have stricter requirements.

There’s also no standard when it comes to debt-to-income ratios. In general, though, lenders like to see a DTI that is below 35% to 45% or so. You may still be able to get approved for a new boat loan even if your DTI is higher than that, just expect that you may need to have one or more of the following:

- A higher credit score

- A larger down payment

- A shorter loan term

The boat loan terms you’re offered can also be influenced by factors like your debt-to-income ratio. The lower your DTI, the lower the perceived risk you pose to a lender. In exchange, lenders may be willing to offer you longer loan terms, smaller down payment requirements, and even reduced interest rates.

What Should My DTI Be for a Boat Loan?

It’s important to note that when analyzing your current debt-to-income ratio, boat loans may have different requirements than other types of lenders.

Again, the specific DTI threshold for your next boat loan will depend on the specific lender and factors like your credit score. The higher your credit score, the higher the DTI you may be able to get approved with; conversely, a lower credit score may result in a lower DTI threshold.

You’ll often find that boat lenders want to stick with a maximum DTI requirement of 45% or less. If your DTI is higher than this, you may have trouble getting approved for your new loan. Also keep in mind that many lenders will look at not just your current DTI, but what your DTI would be with a new boat loan added in.

Curious to know what your monthly payment would be? Check out our boat loan calculator to explore your options.

Ways to Reduce DTI

If your debt-to-income ratio is too high while applying for a new boat loan, you could find yourself on the receiving end of

- Shorter loan repayment terms

- Higher interest rates

- Increased down payment requirements

- Loan application denials

Whether you’ve already started applying for boat loans — and aren’t having the success you wanted — or you’re simply preparing to apply, there are some ways you can reduce your debt-to-income ratio. By doing so, you’ll boost your odds of getting approved for the best possible boat loan.

Pay down some debt. Of course, the easiest way to improve your debt-to-income ratio is to simply eliminate some of that debt. If you have extra cash or savings to throw at existing balances, you may want to pay off an account or two. By doing so, you’ll eliminate the monthly payment associated with that debt and lower your DTI.

Refinance existing balances to adjust your monthly payments. Another option is to adjust the monthly payments you already have, either by lowering your interest rate, extending your repayment term, or both. If your minimum monthly payment is reduced, your DTI will go down as well.

You can often do this with the help of a refinance, balance transfer, or even a consolidation loan. This may be a good option if you’re not able to pay down additional balances at the moment.

Increase your income. Since your DTI is calculated by dividing your monthly debt obligation by your monthly income, you can reduce this percentage by either lowering your debt or raising your income.

Making more money each month will automatically decrease your DTI… but it could be easier said than done for some borrowers. Some possible income-boosting options include:

- Asking for a raise and/or promotion at work

- Taking on a side gig

- Starting a second job in your spare time

While it won’t decrease your personal DTI, another option could be to add a cosigner to your boat loan. Adding a creditworthy co-borrower to your application allows their monthly income to also be considered. As long as this co-borrower doesn’t also have a high level of debt, you could improve your approval odds and even unlock better loan terms.

Ready to see what sort of loan options are available for your next boat? Trident Funding is here whenever you’re ready to apply for a boat loan.