How to Apply for a Boat Loan

So, you’re ready to join the illustrious boat owners club? You can already picture yourself pulling out of the marina, enjoying a nice breeze, and

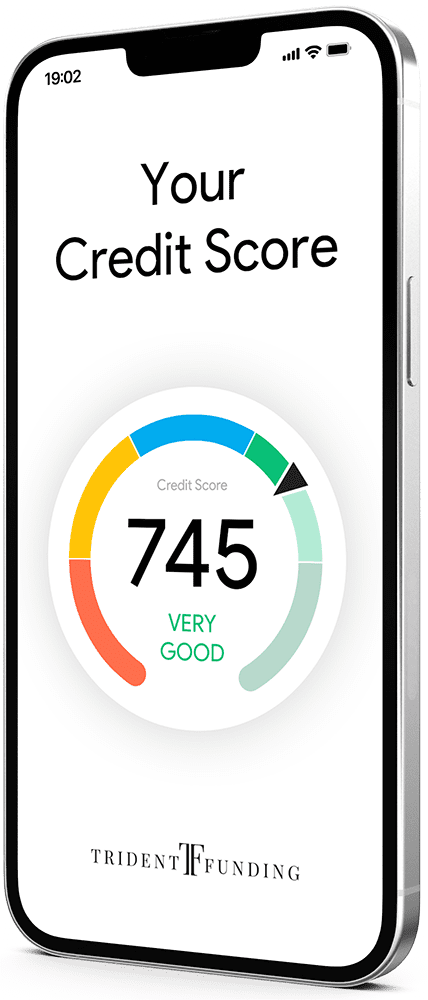

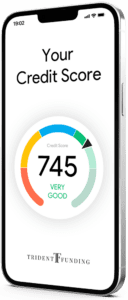

Boat loans aren’t hard to get, but each lender will have their own set of boat loan requirements. You don’t have to have perfect credit or make a million dollars to get a boat loan. You will generally need a credit score of at least 600, enough money for a down payment of 10 to 20 percent of the cost of the boat, and you should be able to prove that you can afford the boat loan payments. If you’re not sure if you qualify for a boat loan, use a boat loan calculator to see how much boat you can afford and your estimated monthly payment.

So, you’re ready to join the illustrious boat owners club? You can already picture yourself pulling out of the marina, enjoying a nice breeze, and

Boat loans are often used by people to finance their purchase of a boat. These loans typically have an amortization schedule that can last for

Consumer interest in boats has grown exponentially in recent years, according to the National Marine Manufacturers Association. This has resulted in record-breaking boat sales, increased

The decision to buy a boat can be one of the most exciting financial moves you make, whether you’re buying a weekend fishing boat or